The dynamic and evolving world of mergers and acquisitions (M&A) offers companies opportunities to:

- Grow exponentially

- Acquire and integrate new and complimentary services or products

- Increase the customer base and enter new markets

- Gain economies of scale and purchasing power

- Dominate segments and industries

However, they also come with complex risks and complicated integration issues that cannot be overlooked. Successfully integrating business operations requires advanced planning, well-coordinated execution, and effective communication. Developing a proper roadmap and identifying resources to efficiently transition to a profitable post-integration state while minimizing risks is critical to achieve transaction objectives.

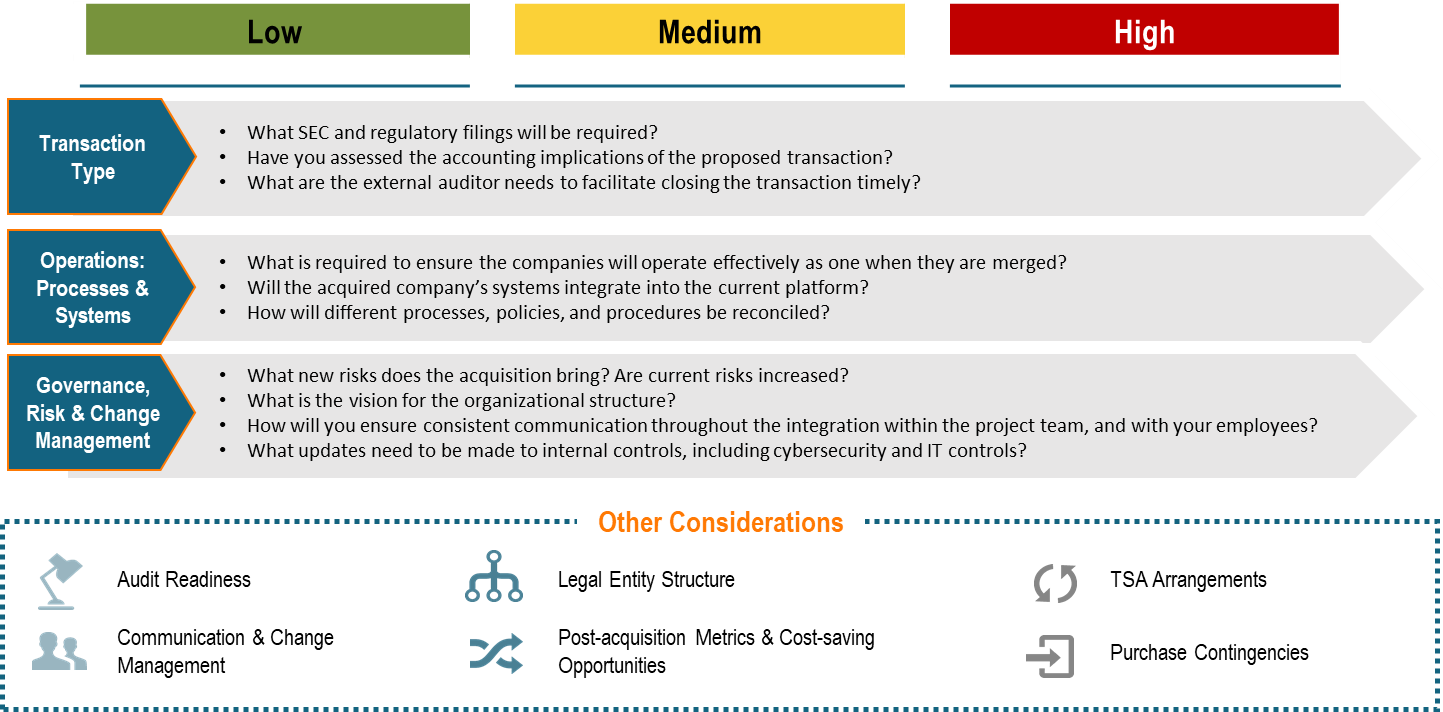

When developing such a roadmap, any organization considering a merger or acquisition must take into account the following questions that influence the complexity of the transaction:

Following, we dig deeper into a key question for each consideration: transaction type; operations; and governance, risk, and change management.

Have you assessed the accounting implications of the proposed transaction?

Any merger or acquisition changes the consolidation of an organization. This requires experience and evaluation of accounting policies, financial reporting implications such as segments and reporting units, financial statement disclosures, and key performance metrics, including non-GAAP financial measures.

Mergers and acquisitions also provide opportunities for the organization to evaluate its current accounting and finance function, to increase efficiencies and potentially automate processes rather than simply replicating the current state. An effective finance and accounting integration plan should include strategies for the following:

- Standardization of corporate finance processes, policies, and reporting requirements

- Consolidation of payroll practices and systems

- Integration of travel and expense polices, systems, and procedures

- Financial forecasting and budgeting for the new entity

- Taxation issues

- Integration of billing, AR, and the general ledger

- Procurement systems and practices

What is required to ensure the companies will operate effectively as one when they are merged?

There are many aspects of a business that need to be included if merged entities will truly come together and achieve the benefits of their newly increased size and synergies. Successful acquisition integrations are founded on strong strategy, attention to people matters, a dedication to speed, and frequent communication to every stakeholder group throughout the process. These processes should be based around a team of dedicated acquisition integration practitioners both at deal-level project management and in functional areas.

To ensure the new company will operate effectively, leadership needs to develop a detailed integration plan that considers all aspects of the business, including:

- Accounting and Finance

- Business Operations

- Client/Customer Support

- Communications (internal and external, including Public and Investor Relations)

- Facilities

- Governance

- Human Resources

- Information Technology

- Legal

- Marketing

- Product Development

- Project Management

- Sales and Sales Operations

- Tax

To ensure that all of these functions are addressed, leading companies know that it is important to formally create an integration governance structure that will focus executive time and talent on obtaining the strategic synergies of a combination. Merely putting people into transition or implementation management positions does not alone keep a merger on a successful course. It requires an effective structure, able leadership, and systematic processes to make progress. This means molding individual contributors into transition teams and helping them handle the many operational and political factors that can otherwise transform good ideas into bad practice, and great opportunities into painful memories.

An organization’s integration structure should include: an M&A steering committee to provide strategic input and help clarify issues, a business sponsor to give guidance on any decisions required by the integration team, an integration leader to provide overall direction of the integration process, an integration project manager who is responsible for the day-to-day project management of the integration, and representatives from the functional areas listed above to provide input and support throughout the entire integration process.

What is the vision for the organizational structure?

When integrating two companies, leaders cannot ignore key change management questions:

- How will you integrate the cultures of the two organizations?

- How will the integrated company’s organization merge with the existing structure?

- How will the reporting relationships change?

- What is the impact to human resources processes such as performance management, compensation, promotion, and career mentoring?

- Are there different operating models, such as decentralized processes versus a shared services model, that need to be reconciled?

Failure to consider these questions can lead to attrition, lost productivity, and integration delays.

A well-executed integration will provide a great opportunity for a business to grow strategically and exponentially. To achieve these benefits, management needs to begin by assessing how complex the merger or acquisition will really be. Doing so will help to prevent disruption, delay, additional cost, as well as employee, board, and customer frustration. An effective and honest assessment utilizing the matrix above will help the company to successfully achieve its M&A objectives.